Investeer

Over

Kennis

Maak kennis met Valvest: dé manier om eenvoudig te beleggen in vastgoed. Kies uit zorgvuldig geselecteerde projecten, profiteer van een lage instapdrempel en laat ervaren experts het werk voor je doen. Ontdek vandaag nog hoe Valvest beleggen simpel en toegankelijk maakt!

Bronnen

Terug

Spain’s housing market in 2025 is showing robust growth tempered by persistent supply constraints. Demand continues to outpace development activity, pushing prices upward and creating both challenges and opportunities for investors and developers. This blog examines nationwide trends, zooms in on major cities, compares real estate dynamics across Madrid, Barcelona, and Valencia. Backed by official data, we conclude with a broad outlook for the year ahead.

Spain’s housing development market is under intense pressure as demand far exceeds supply. According to the Instituto Nacional de Estadística (INE), approximately 246,000 new households form annually, yet only 85,000–90,000 new homes are completed each year. This gap, unchanged from 2024, with new home completions dropping slightly (-0.4% year-over-year in January 2025, per the Ministry of Housing), is fueling price increases across the country.

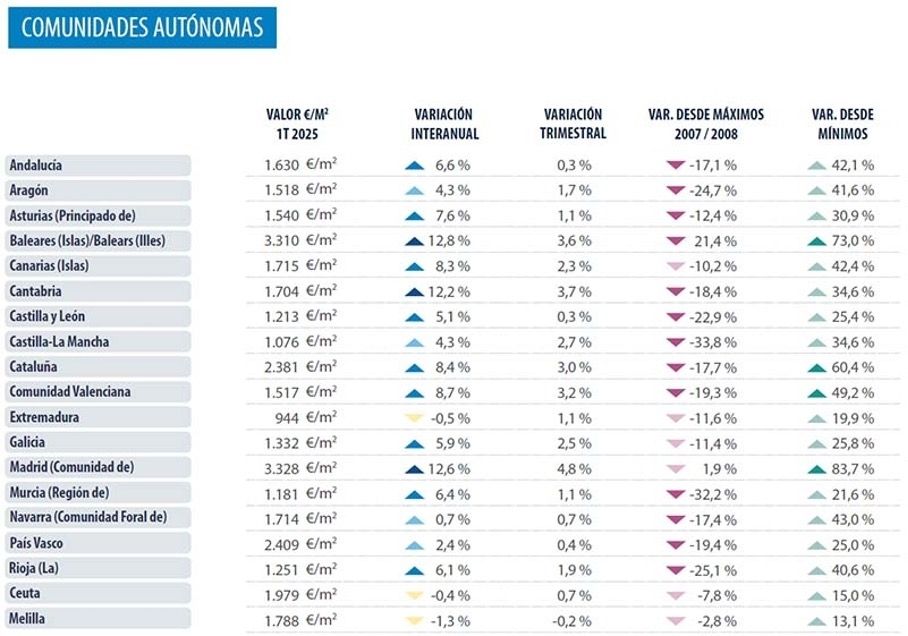

The Ministry of Housing (MITMA) reports that house prices rose in 18 of 19 autonomous regions in 2024, with annual growth ranging from 4% to 9% in most areas. Standout performers include:

Quarterly gains further highlight the trend, with Madrid (+4.8%), the Balearic Islands (+3.6%), Comunidad Valenciana (+3.2%), and Catalonia (+3.0%) leading the charge.

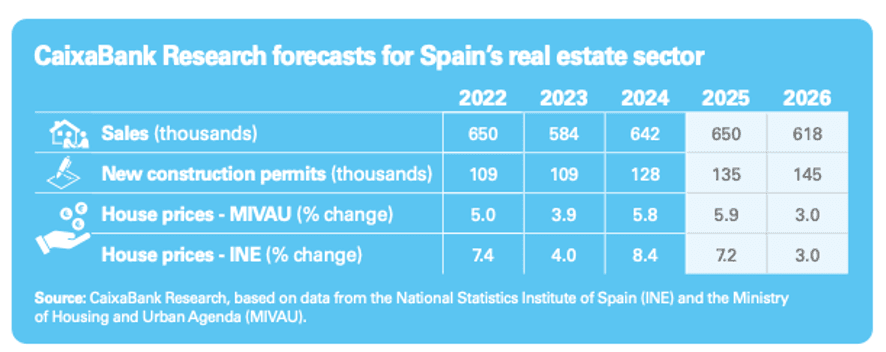

CaixaBank Research forecasts a continued boom through 2025–2026, driven by several tailwinds:

They predict 650,000 housing transactions in 2025, easing to 620,000 in 2026 as temporary demand drivers, like pent-up demand from 2022–2023 and falling rates wane. On the supply side, new construction permits are projected to climb to 135,000 in 2025 and 145,000 in 2026. However, this remains well below household formation rates, sustaining price growth at 2024 levels into 2025. For 2026, price increases may moderate as supply inches upward, though the accumulated deficit will keep affordability challenges alive. A slower supply response could amplify price pressures further, depending on demand dynamics.

Spain’s major cities are the epicenter of both opportunity and constraint. Madrid and Catalonia (home to Barcelona) are seeing explosive demand, with annual price growth nearly doubling from the prior quarter Madrid at 4.8% and Catalonia at 3.0% in Q1 2025. Job growth, tourism, and foreign investment are key drivers. In Q1, Madrid’s property prices hit €4.400/m² +/-, while Barcelona’s reached €4.735/m² (Idealista). Yet construction struggles to keep up: Madrid issued 8,000 new permits in 2024, and Barcelona around 5.000, far short of what’s needed to meet household formation and tourism-driven demand. Land scarcity and regulatory bottlenecks push developers toward high-end projects or renovations rather than affordable housing.

Valencia, within Comunidad Valenciana, is emerging as a development hotspot. With a quarterly price rise of 3.2% and an annual increase of 8.7%, prices reached €1,650/m² in 2024, significantly lower than Madrid or Barcelona. This affordability, paired with strong demand, attracts developers, though only 3,500 new permits were issued in Valencia province last year, highlighting supply limitations.

To better understand Spain’s urban housing dynamics, let’s compare Madrid, Barcelona, and Valencia across key metrics from platforms like Idealista, MITMA and Caixabank.

Price Levels (2024):

Annual Price Growth (2024):

Quarterly Price Growth (Q1 2025):

New Construction Permits (2024):

Key Drivers:

Challenges:

Madrid offers the strongest short-term price momentum, Barcelona commands the highest prices with a tourism edge, and Valencia stands out for affordability and growth potential—making it a sleeper hit for 2025.

The holiday rental sector remains a bright spot, particularly in Valencia. With an 8.7% annual price rise and yields outpacing many regions, the city is a magnet for investors. However, new legislation in Comunidad Valenciana, introduced in late 2024, tightens rules on short-term rentals, requiring licenses, limiting permits in saturated areas, and enforcing stricter compliance. While this may cool investment, it could stabilize long-term returns by curbing oversupply. Short stay properties that already hold a tourstic licenses remain uneffected and can continue to rent out.

Spain’s housing development market in 2025 blends opportunity with constraint. Nationally, prices are soaring—led by the Balearic Islands (+12.8%) and Madrid (+12.6%), but construction remains flat, hampered by land shortages and a completions rate of just 85,000–90,000 homes against 246,000 new households. Major cities reflect this tension: Madrid’s rapid price surges, Barcelona’s premium market, and Valencia’s affordable growth potential highlight diverse investment prospects. Holiday rentals, especially in Valencia, offer high yields despite regulatory shifts. For developers and investors, success hinges on adaptability, navigating tight supply, regulatory changes, and targeting high-growth areas like Valencia’s emerging neighborhoods. With 650,000 transactions forecast and supply slowly rising (135,000 permits in 2025), the market favors those who can act decisively in this dynamic landscape.

Maak een account aan en begin met beleggen in vastgoed

Invertir en el sector inmobiliario solía ser difícil y complicado.

En Valvest, nuestra misión es poner la inversión inmobiliaria al alcance

En Valvest, realizamos todo el trabajo internamente para lograr la máxima calidad y eficacia. Desde el principio hasta la finalización de un